The Beginner’s Guide to Health Savings Accounts (HSAs) and How They Work

Imagine saving money for doctor's visits and still cutting your taxes three ways. That's the magic of a Health Savings Account, or HSA. This tool beats out old-school options like FSAs because your cash rolls over year after year. You get tax breaks on putting money in, watching it grow, and pulling it out for health costs. If you're new to this, stick around—I'll break down how HSAs work and why they shine as a top pick for your wallet and well-being.

Section 1: What Exactly is a Health Savings Account (HSA)?

A Health Savings Account lets you set aside pre-tax dollars for medical bills. It's paired with a high-deductible health plan to keep premiums low. Think of it as your personal health piggy bank that grows over time.

Eligibility Requirements: Who Can Open an HSA?

You need a High Deductible Health Plan, or HDHP, to qualify for HSA eligibility. For 2026, the IRS sets the minimum deductible at $1,650 for individuals and $3,300 for families. Out-of-pocket limits cap at $8,300 for one person or $16,600 for families—check the latest on IRS.gov for exact figures.

No other health coverage can overlap, like Medicare or a general health plan. If you're enrolled in an HDHP through work or on your own, you're good to go. Self-employed folks often find this setup saves big on premiums.

The Mechanics: Contributions and Ownership

Anyone eligible can add to their HSA—you, your boss, or both. For 2026, the cap sits at $4,300 for individuals and $8,550 for families. Those 55 and older get an extra $1,000 catch-up amount.

The best part? You own the account forever. Job changes don't touch it. Funds stay yours, building a safety net no matter where life takes you. This portability makes HSAs a smart long-term choice.

Comparing HSAs to FSAs and Health Insurance

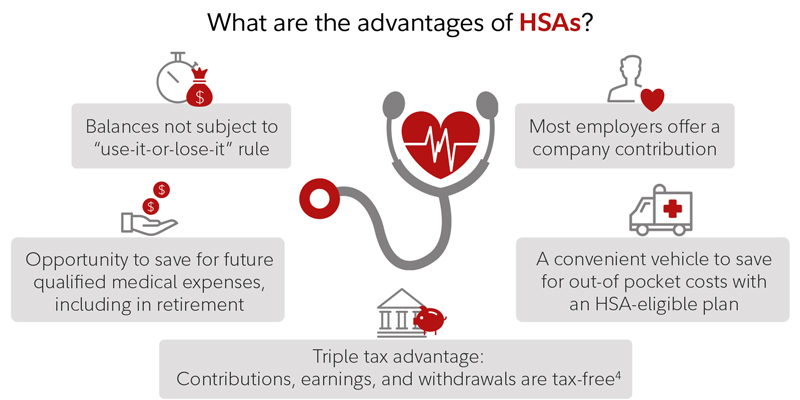

HSAs stand out from Flexible Spending Accounts because money doesn't vanish at year-end. FSAs force you to use funds by December 31, or lose them. With an HSA, leftovers carry forward, giving you real flexibility.

Health insurance covers routine care after deductibles, but HSAs focus on out-of-pocket hits. Here's a quick side-by-side:

- HSA: Rollover allowed; investable; owned by you.

- FSA: Use-it-or-lose-it; no investments; employer-tied.

- Traditional Insurance: Lower deductibles; higher premiums; less tax perks.

For HSA vs FSA debates, the winner is clear if you hate wasting cash. HSAs fit better for unpredictable health needs.

Section 2: Understanding the Triple Tax Advantage

The real draw of an HSA explained comes from its three tax wins. You dodge taxes coming in, while growing, and going out for health stuff. No other account stacks up like this—it's like free money on steroids for your medical future.

Tax Deduction on Contributions (Tax Break 1)

Put cash into your HSA before taxes hit, and it lowers your taxable income right away. If your salary is $50,000 and you add $4,000 via payroll, your adjusted gross income drops to $46,000. That means less owed to Uncle Sam.

Even direct deposits count—you deduct them on your tax return. This perk shines for self-employed people who skip payroll setups. Save hundreds yearly without extra hassle.

Tax-Free Growth (Tax Break 2)

Once inside, your HSA money can invest in stocks, bonds, or mutual funds. Earnings compound without a tax bite, just like a 401(k). Unlike Roth IRAs, no income caps block you from this growth.

Most providers offer easy options: savings accounts for safety or brokerage links for more risk. Over 20 years, $4,000 invested at 7% could double twice, all tax-free. This turns your HSA into a powerhouse for later years.

Tax-Free Withdrawals for Qualified Medical Expenses (Tax Break 3)

Pull funds for approved health costs, and no taxes apply—ever. Qualified HSA expenses include doctor visits, prescriptions, dental work, and even some over-the-counter meds, per IRS Publication 502.

Save receipts from any time in your life. Reimburse yourself decades later, tax-free. This lifetime access beats time limits on other accounts. After age 65, non-medical pulls just face income tax, no penalty.

Section 3: Utilizing Your HSA: Spending vs. Saving

Decide if you'll tap your HSA now for bills or let it sit for the future. Both paths work, but planning ahead maxes the benefits. Balance current needs with long-term goals to stretch every dollar.

Paying for Current Medical Costs

Use your HSA debit card for co-pays or pharmacy runs. It feels like cash, but with tax perks. Track every spend—apps from providers make this simple.

A smart move: Pay bills from your regular bank, then reimburse from HSA later. Keep that receipt safe for years. This keeps your invested funds growing while covering today's hits.

The HSA as a Long-Term Retirement Vehicle (The "Stealth IRA")

Treat your HSA like a hidden IRA for health in old age. Let it grow past 59½ without touching it. Medical costs skyrocket after 65—Medicare doesn't cover everything.

High earners love this: Max contributions now reduce taxes, then withdraw tax-free for retirement healthcare. Say you sock away $8,000 yearly for 30 years at 5% return. That could hit $500,000, slashing future bills and taxes. It's stealthy because it flies under the radar of typical retirement talks.

Understanding Penalties for Non-Qualified Withdrawals

Before 65, non-medical uses cost you: full income tax plus 20% extra. Ouch—that's like throwing away a fifth of your savings. Stick to health needs to avoid this trap.

After 65, the penalty drops. Non-health pulls just get taxed like regular income. Plan wisely, and your HSA becomes a flexible retirement booster without the sting.

Section 4: Managing and Maximizing Your HSA

Pick the right setup, contribute smart, and watch your account thrive. Small choices here pay off big. Stay on top of rules to avoid surprises.

Choosing the Right HSA Provider

Look for low-fee banks or brokers like Fidelity or HSA Bank. Check debit card ease and app features for quick reimbursements. Investment menus matter—opt for ones with no trading costs.

If your job picks the provider, ask about their options. Some offer great funds; others stick to basic savings. Shop around if you're independent—fees under 0.5% keep more in your pocket.

The Best Time to Contribute: Payroll Deduction vs. Direct Contribution

Payroll pulls trim your paycheck taxes instantly. No waiting for tax time. It's hands-off and builds the habit.

Direct adds work too, but claim the deduction in April. Pick payroll for simplicity unless you're tweaking your budget mid-year. Either way, start early to hit limits.

Strategies for Maximizing HSA Contributions Annually

Spread deposits monthly to avoid a year-end rush. If 55+, add that $1,000 catch-up before December 1. Keep your HDHP active all year—losing eligibility cuts contributions short.

Automate transfers to never miss out. Families, coordinate with spouses to double up without overlap. Aim for the full $8,550 in 2026; it's like free tax shelter. Track via IRS forms to stay compliant.

Conclusion: Taking Control of Your Healthcare and Financial Future

HSAs offer unmatched perks: triple tax savings, easy moves between jobs, and growth potential. They're more than a bill payer—they build wealth against rising health costs. Start one today to secure your path.

Here are the top three facts for beginners:

- You need an HDHP to open an HSA, with 2026 limits at $4,300 individual contributions.

- Enjoy tax breaks on deposits, earnings, and qualified medical pulls—no other account does all three.

- Let it grow for retirement; after 65, it's like a flexible 401(k) for any need.

Ready to unlock your HSA? Talk to your HR team or visit IRS.gov to get started. Your future self will thank you.